Published On - February 16, 2023

Next in DeFi? Collateralised Securities

Stablecoins are a cornerstone of the DeFi ecosystem providing crypto natives with on-chain dollars, not subject to the wild volatility of native cryptocurrencies (provided they’re fully collateralised). However, there’s no reason why this collateralised model cannot be applied to a much wider range of financial assets. For instance, securities. This is exactly what a project named Backed has done.

Bringing the S&P 500 on-chain

There is now a token available on Ethereum which tracks shares in an S&P 500 ETF (specifically, the iShares Core S&P 500 UCITS ETF (CSPX)). The token is named bCSPX (Backed CSPX), of which there are 100 tokens with the standard 18 decimals of precision for an ERC-20 contract. These tokens represent a maximum issuance of $100m according to the final terms database. Although the issue volume is up to CHF 100m according to the legal terms . This is because the issuer, Backed Assets GmbH is based in Switzerland and complies with the Swiss DLT Act.

bCSPX token details

bCSPX token details

The fees taken by the underlying investor are stated as up to 0.5% of the marketplace of the underlying ETF. As the underlying is a regular ETF, it's relying on traditional financial markets asset infrastructure including its broker, security agent and custodian.

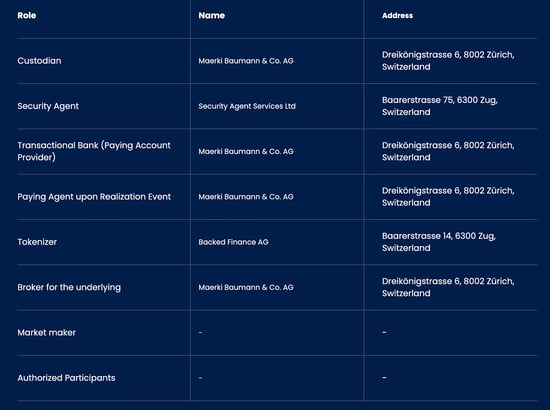

Traditional financial service providers support the bCSPX token

Traditional financial service providers support the bCSPX token

Whilst this goes against the idea of a fully native DeFi asset, this playbook is likely to be the most viable approach to driving widespread adoption of DeFi technology in finance.

For years its been discussed how blockchain, crypto and DeFi can impact financial services. But it's been difficult to comprehend what this disruption looks like. Fully collateralised on-chain assets seem like a likely route forward. Any organisation holding significant currency reserves could issue a stablecoin. Exactly the same logic applies to securities. If banks are starting to tokenise deposits to issue stablecoins, why couldn't we see the same thing happen with issuers of securities?

A new distribution platform for TradFi

There's already a multitude of platforms offering asset tokenisation services, but what we have yet to see is the availability of public market securities on blockchains. Public blockchains are effectively a new distribution platform for these assets. Currently, retail investors have to go through a broker to access them, be that a broker in the traditional sense or a fintech platform such as RobinHood.

There are two beneficiaries of this:

- Firstly, any assets that are available on a public blockchain have a global reach. We've seen how transformative access to stablecoins such as USDC is in the developed world, and the same could happen with securities too. Enabling anyone globally to hold an ETF tracking the S&P 500 greatly democratises access to financial products.

- Secondly, the programmable nature of blockchain assets will create many new opportunities for innovation. What's there to stop developers from creating self-managing composable portfolios of equities or ETFs that are managed entirely via smart contracts?

We've seen many of the world's largest brands and artists embrace NFTs to provide a new channel to engage with their customers and fans. Issuing fully collateralised assets on public blockchains is an equivalent opportunity for the financial services industry.

At the current time, organisations such as Circle and Backed are positioning themselves for providing the services to bring different financial assets on-chain. If we put regulatory hurdles aside, is there a reason why exchanges could not potentially offer such products to retail investors?

Given the success of stablecoins in DeFi, it is logical that something similar will emerge for securities . Where those that gain significant traction are assets that bridge the old world and the new. They don't declare the traditional financial world as completely broken but instead find ways to bridge it with the new.

This is good for users, as the existing trust and relationships that have been established can be leveraged to onboard new users to these blockchain-enabled assets, rather than simply declaring the existing antiquated. We need to lower the barriers to entry for certain financial products and established entities such as banks and exchanges are well-placed to offer this.

Parallels with the world wide web

This has parallels with what we saw with the world wide web. When the web started out, it was simply a repository for information, there wasn't a clear path to monetisation for many companies. However, as more users were onboarded and the tools for engaging with websites (browsers) become more familiar, we saw companies establishing their web presences as it became another mechanism they could reach their customers via.

Smartphones and app stores also played a part here, but the point was that the internet enabled companies to streamline their relationships with customers and ultimately services moved from offline to online .

With on-chain fully collateralised securities and decentralised exchanges, issuers have the opportunity to offer assets directly to investors bypassing traditional brokers and investment platforms. This significantly streamlines some of our modern financial infrastructure.

Wholesale finance

The model offered by Circle and Backed is simply a distribution channel for currencies and ETFs. It doesn't in any way influence or modify the assets they represent. They are financial products made available on blockchains. While it isn't just retail investors accessing crypto markets, I think it's fair to consider these types of products as being retail focused.

They are underpinned by assets that are managed in wholesale financial markets, and exactly how blockchain will impact these, is still less certain.

Internet technologies were embraced within wholesale finance via private networks, with strict onboarding controls. Websites and apps were mainly embraced for retail focussed financial products. It is possible that we will see the same thing happen with blockchains, where wholesale networks remain on permissioned blockchain rails, with retail offerings made available via public blockchain rails.

Trusting public networks

Blockchain technology will be used throughout financial market infrastructures, but it will be challenging for larger nations to prioritise building on top of public networks due to the decentralised trust that they enforce.

Instead, public blockchain networks may end up serving as a mutual trust layer for bridging between different jurisdictions for private networks . Whether it plays out this way remains to be seen.

However, in the nearer term, we're going to start seeing a lot more financial securities showing up on-chain, and this will help catapult the TradFi industry onto web3.